Perceptions during the Swiss Crisis

Origins of collective memory in the misapprehensions of 1975-1983

The crisis

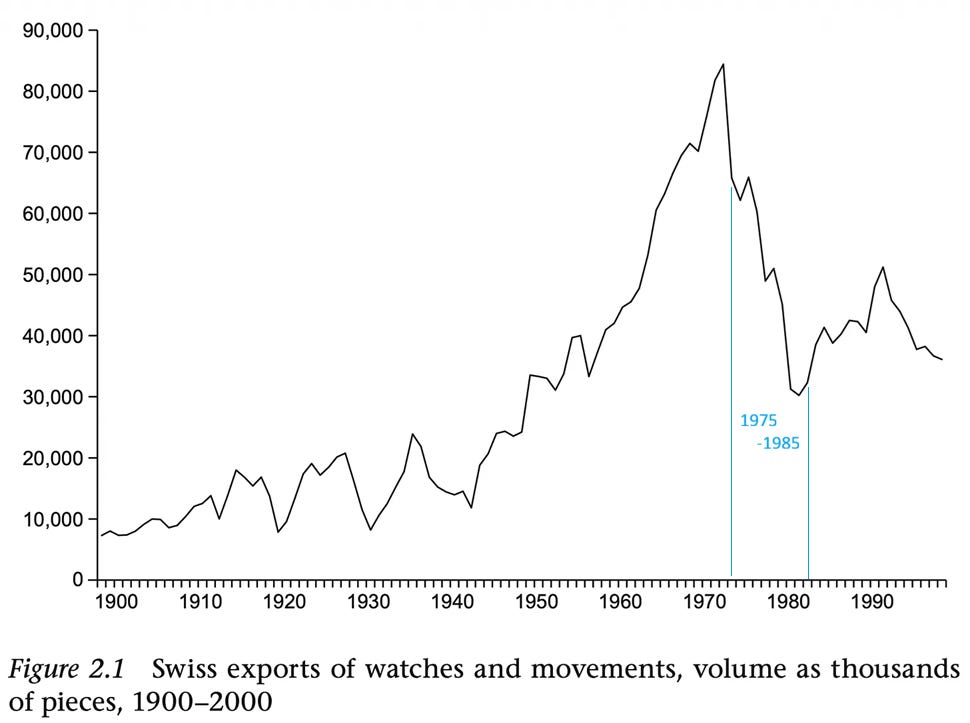

In 1975, the number of Swiss watches exported suddenly fell by a fifth from 1974’s all-time high of nearly 90 million watches. This number had risen without much interruption since the 1930’s Great Depression.

The grinding years following left no doubt that the industry was in deep crisis, stretching into a yearslong ordeal during which it permanently lost its dominant volume share of the world watch market.

Actual causes

Pierre-Yves Donzé’s The Business History of the Swatch Group (highly recommended) takes only 24 short pages to rigorously establish that the crisis of 1975 to 1985 was because of the failure of the industrial structure to keep up with production efficiency gains at its American, Japanese and Southeast Asian competitors.1

He demolishes the notion that the cause lay in the emergence and democratization of quartz watches.

Donzé summarizes: “More than a product innovation, a process innovation was indeed at the heart of the lost competitiveness of the Swiss watch industry in the years of crisis between 1975 and 1985.”

US case study

Then, as now, the US watch market was the single largest in the world. While the import value of Swiss watches grew significantly in absolute value terms even during 1975-1985, import value from Japan grew by more than 20 times during the same period.

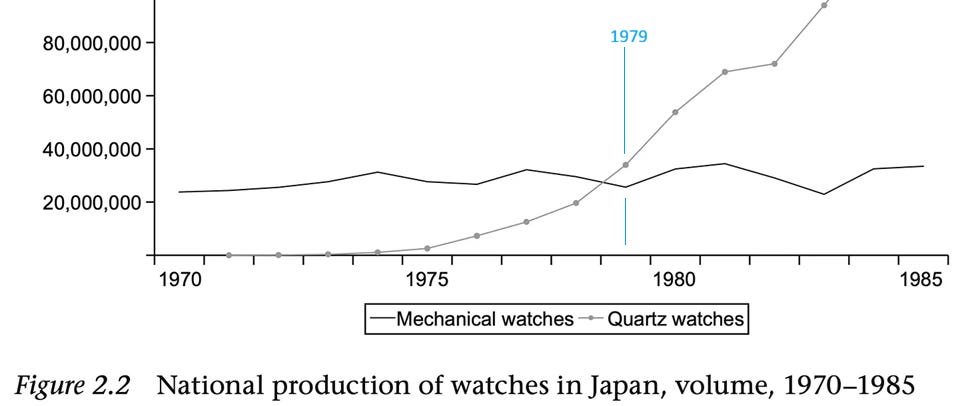

Japanese mass production evolved within its domestic market well before the introduction of quartz watches, with Suwa Seikosha alone in 1970 producing 14 million mechanicals, equal to a fifth of Swiss production. Japanese quartz production units did not surpass mechanicals until 1979, at about 25-30 million of each type.

During the crisis, therefore, the Japanese watches rapidly penetrating into the US2 were both mechanical and quartz models. Imported Japanese watches surpassed Switzerland by 1978 by value, and even earlier by units.

US firm Timex also made major inroads. Donzé writes that Timex, by mass producing mechanical watches, “occupied the bottom end of the range [in the market] until the late 1970s, when they were replaced by cheaper quartz watches.”

In contrast, “although Swiss companies had mastered the technologies for the mass production of watches in the 1960s, with the exception of [Rolex], they did not adapt them to the manufacture of high-quality goods. There was a real gap between quality watches, where production was not streamlined, and cheap, mass-produced watches, with both production systems coexisting sometimes within the same company.”

In any other industry, the market share trajectory of a production cost differential is fairly predictable.

Industry perceptions during the crisis

This article is not about causes.

The subject here is what people thought at the time. A future article might then look into how the crisis was remembered afterwards.

Sources are the trade publications such as Europa Star, La Suisse Horlogère, and Revue FH. The assumption is that these reflect the thinking of the wider industry.

Brief chronology

1973: Arab Oil Embargo; plethora of quartz showpieces at Basel; Fr.1,000 = $310

1975: Stagflation; height of digital watch mania; Swiss exports crash; Fr.1,000 = $380

1977: End of LED; OysterQuartz 17000; Fr.1,000 = $480

1979: Iranian Revolution; analog favored over digital quartz; JLC and IWC rescued by VDO; Fr.1,000 = $625

1981: World economic slump; Plaza Accord; stronger yen; Fr.1,000 = $550

1983: SSIH and ASUAG merger into SMH/Swatch; fashion watches; Fr.1,000 = $450

Attention to the ‘electronic watch’

It cannot be understated how fixated the 1970s and early 80s Swiss industry was on the electronic watch, especially after the 1973 Basel Fair. Electronic watches had long been anticipated in Switzerland as a commercial opportunity.

Bulova had the Accutron. It was not for nothing that tuning fork movement inventor Max Hetzel was recruited back to Switzerland in 1963 to develop equivalent ‘Swissonic’ technology which did not infringe on Bulova’s patents.

The bimonthly Europa Star editorials of the 1973-1983 period are filled with think pieces on, variously:

‘the future of the watch’ including serious debate on the mechanical watch eventually going extinct3

the entry of American electronics giants, some as collaborators and others as competitors

the ‘solid state’ watch with electronic display, particularly le affichage digital 4, including the potential for liquid crystal displays (LCD) as contrasted with the early failure of LED

the hope for a Swiss comeback based on cheaper-to-make and/or technologically superior quartz watches5

advances in quartz thinness, battery life, accuracy, functionality, etc.

the growth of the quartz share of Swiss exports, which reached 20% in 1980

Then there are the copious advertisements of not just watches but quartz movements, crystals, motors, and batteries.

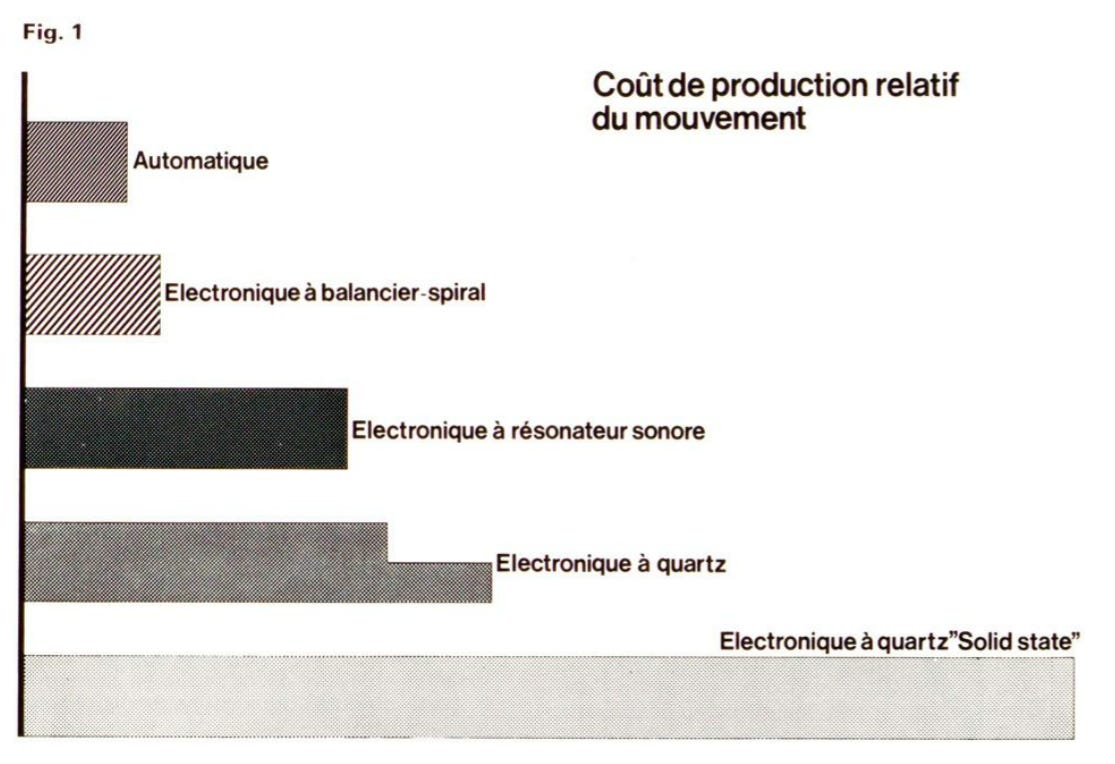

Quartz was seen as a great sales opportunity that brands did not want to miss, obliging ASUAG’s Ebauches SA unit, the quasi-monopoly supplying movements to a majority of brands at the time, to publish a 1973 manifesto outlining its strategy. “We realize that we have a duty to our customers, that of investigating all the possibilities of modern electronic development,” it said, followed by a chart of relative costs of movement types, with analog quartz indicated to cost between 3.6 to 4.5 times a ‘medium quality’ automatic.

The immediate goal was succinctly stated: “a quartz-crystal watch which will sell at a reasonable price, while offering such a high degree of accuracy that its owner will not have to reset it during the lifetime of its battery, which supplies sufficient power for at least one year.”

Then, reflecting 1973’s widespread expectation that analog quartz watches would be a transitional product type, Ebauches said “the mechanical watch will continue to exist for many years to come,” then skipping over analog quartz to say that, in the field of digital watches, “the future holds in store for us new models of the greatest interest.”

Not to be outdone, SSIH released a statement the following spring:

Who amongst the public could have foreseen a few years ago the radical upheaval in concept that watches were about to encounter? It was anticipated however by a small number of dynamic concerns [e.g. us].

The fact that Omega is in a position to market the varied range of watches just described, is due to the constant research and development of the group to which it belongs: the S.S.I.H. (for «Société Suisse pour l’Industrie Horlogère S.A.»). This company which is the third [largest] producer of watches in the world and the foremost in Switzerland, has always designed and manufactured its own calibers. Developments in the last few years therefore led it to become a real electronics company so as not to renounce that policy.

It took util 1978 for the novelty to wear off. By then, even Rolex had released its in-house Oysterquartz6, and Piaget its ultrathin cal. 7P. The analog watch had been identified as the commercially promising avenue for premium quartz. From the quartz products which emerged in subsequent years from brands as diverse as Omega, Eterna, Zenith, Longines, Patek Philippe, JLC, Heuer, Ronda, Girard-Perregaux and F. Piguet, we can surmise that multiple quartz development projects were in progress across Switzerland.7

Therefore, for much of the crisis, Swiss industry focused on developing new product technology, perhaps hoping to maintain a pricing edge by technology. By and large, it neglected updating its manufacturing or process technology.8

However, ‘quartz’ was not the only matter occupying minds, for the benign international environment taken for granted since the 1950s was no more.

Attention to external events

In between articles on quartz, a second recurring subject in editorials was the exchange rate of the Swiss franc, and later even the tides of the watch-importing economies. To recall, Richard Nixon ended dollar convertibility to gold in the summer of 1971, precipitating the end of fixed currency exchange rates (rates which happened to favor Swiss exports), setting off a multi-year rebalancing of national economies.

Europa Star editor Valentin Philibert, writing as Swiss exports were crashing in 19759, framed it as a complete surprise:

The economic depression that had been taking hold in the world’s industrialized countries since 1973, closely following the inflationary surge of the previous decade, had spared the watch industry in Europe until the beginning of the second half of 1974. On the contrary, 1973 sales figures were exceptional, particularly in Switzerland and France, and 1974 was shaping up to be even better.

And then suddenly, like lightning on a summer’s day, the crisis struck the watchmaking industry. Switzerland was particularly hard hit because it was in the midst of expansion [of watchmaking capacity], and its industry, which had enjoyed an impressive number of prosperous years and was engaged in a complex restructuring process, was hardly prepared to withstand such a shock.

This reflected the industry perception. Exchange rate concerns recur repeatedly, raised for example by the leaders of FH and GP.

Others pointed out that warning signs had been ignored. “The first signs were already apparent in 1973,” attendees of the 100th anniversary celebrations of the Swiss Watch Chamber were reminded.10

In 1978, as the Swiss franc was on its way to doubling in dollar value11 compared to 1973, Philibert lamented that: “all the efforts made in recent years which, in normal times, would have carried it to the highest summits, are now like windblown straws in the face of the currency storm.”

Industry later saw, however, that the Swiss franc reversing course to a weakening trend after 1981 did not help much. An automated factory is not just twice as efficient; it can be 4 or 8 times.

Underestimating the competition

Worldwide watch sales continued to grow during the crisis years, but were supplied mainly by the growing exports of competitors, such as Japan and Hong Kong.12

For a brief period, a theme was about how the competition was less financially disciplined, less ethical, or simply less serious.

Using a shock strategy they had employed with success in other spheres, American electronics concerns did away with the best established traditions…

There is room for everyone in this sector so long as the great horological traditions of good workmanship and business honesty are respected.

editorial, Europa Star Europe | 1976 | Issue #98

At the height of the craze for high-end digital watches:

Will these ‘amateurs’ be able to continue thwarting the expansion of serious manufacturers in Europe, America or the Far East? We do not think so because the wheat is separated ruthlessly from the tares and of the many that are called, only a few are elected; those that have proved their determination and know-how…

editorial, Europa Star Europe | 1975 | Issue #91

The mid-70s American foray was given special ire in a 1982 retrospective: “Seeing a vast potential market, the Americans flooded the horological world with calibers each one more sensational than the last and equally transient.”13

Relatively few writings can be found to the effect of “they were more efficient.” What seemed to dominate when thinking of the competition was a certain emotional reaction, tending to preclude cool consideration of what it would take to compete against newcomers.

Why emotion? In the historical record, one factor stands out.

Resentment at being called obsolete

Even before there was a commercial crisis, excitement about the new electronic technology overshot into predictions that the mechanical watch was obsolete. This naturally caused some resentment, especially among those who had invested considerable time and effort in the craft.

Among them was George Daniels, who in a 1999 BBC interview recalled:

I was first provoked to make watches by the introduction of the quartz watch, and all the adulation that followed this, mainly directed towards encouraging the public to believe that the mechanical watch was dead, and this was the new era of electronic timekeeping, and the only way forward.

And I was furious because I’d spent all my life devoted to mechanical watches, and now these damned electricians have come along and tried to tell me that they could do it better.

As the devastation of a halving of unit exports (1974 to 1980) spread across watchmaking towns, some even advocated for Switzerland to transition to 100% quartz watchmaking (which represented the higher price point), while shifting mechanical watch production abroad.

A 1980 Europa Star editorial reported that the underlying premise was largely accepted. “No objections were raised against the transfer of technology in principle.”

Such is the power of groupthink. Surely there were many independent thinkers silently seething.

Emotion, even justified, clouds judgement.

(In)attention to changes in process;

industrial structure taken as a constant

Some commentators correctly diagnosed that the Swiss industrial structure needed reform, but underestimated the degree necessary. A 1977 Europa Star editorial referred in the past tense to “profound structural changes. Production was firmly re-organized.”

What is largely absent is commentary about the inefficiencies of, and the lacking (or even perverse) incentives in, the system itself.

Swiss watchmaking entered 1975 still very dependent on economical and midpriced watches. The main underlying supplier, Ebauches S.A., enjoyed a quasi-monopoly status which shielded it from competitive pressures. In a monopoly, there is more incentive for managers to play safe than to take risks e.g. advocating for large investments in automated production. Which might even threaten jobs.

Then, in the premium segment, was there a belief in the marketing fiction of “it costs as much as it costs and it takes as long as it takes” which might only apply in tier above? Donzé cites Rolex as the sole exception. Was ‘efficiency’ a dirty word everywhere else?

Unfortunately, crisis Switzerland was far from being specialized in luxury watches, and the reality of that segment, even to this day, is that the vast majority of ‘luxury’ brands serve a price-sensitive clientele, having at their disposal many alternative ways to spend their money.

Ebauches and the proud SSIH were also insulated from financial discipline, enjoying a certain leeway with Switzerland’s largest banks. National champions “too big to fail.” It took the deep world economic crisis which began in 1981 to force a final reckoning.

The worst crisis since The Great Depression

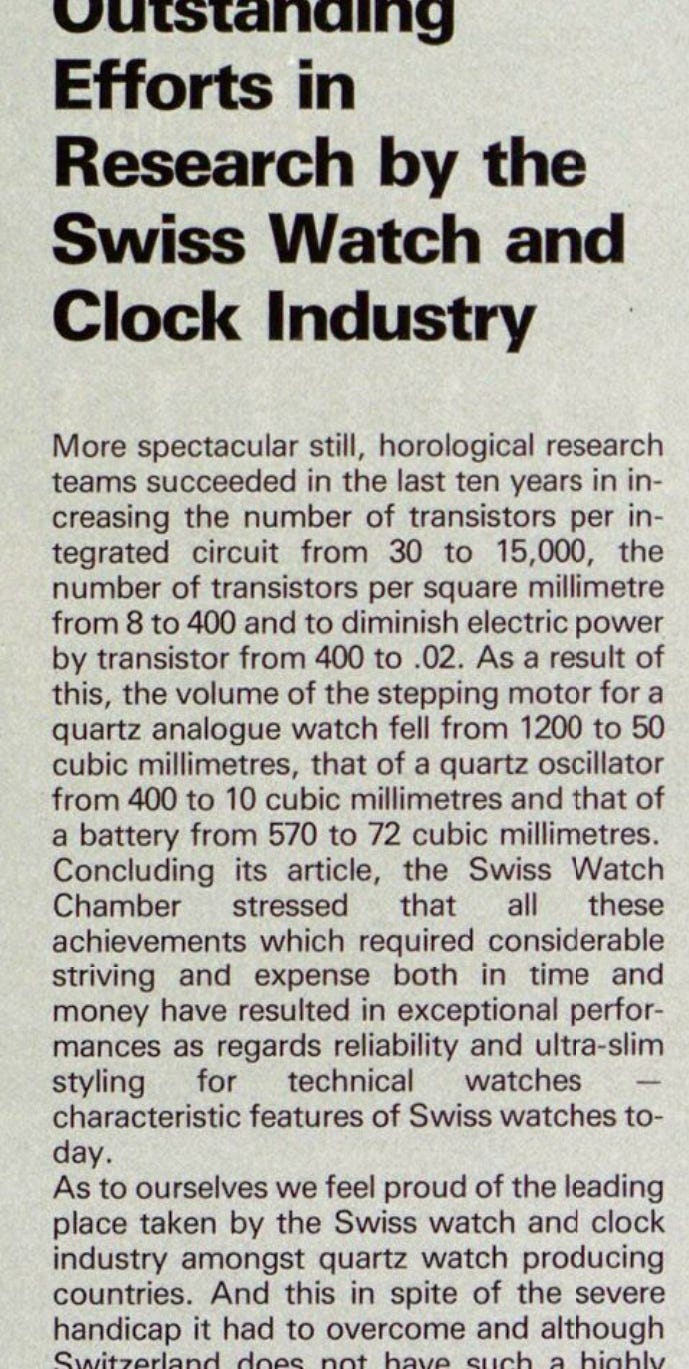

Swiss industry closed 1980 thinking that the worst was over. Still reflecting the pro-quartz focus, the Swiss Watch Chamber celebrated ten years of electronics R&D with a list of impressive technology statistics

The good times were short-lived. By 1981, Paul Volcker’s inflation fight saw 20% interest rates. The world joined the US in an economic malaise which drove consumers to lower priced watches, when they bought at all, which were by then overwhelmingly not Swiss Made. Worse, the sudden turn in demand induced a large inventory overhang at the distribution and retail level, further depressing orders to watch factories.

By the eve of the 1983 Basel Fair, only jewelry and fashion watches were optimistic. Gone was the hope of just two years prior that superior technology would save the day for Swiss watches. Currency winds were favorable, yet the industry was bleeding out.

The gloom was total, with Philibert writing morosely:14

Everything seems to have been in league to destroy the very foundations of what was once a flourishing and seemingly indestructible industry. The inrush of electronics, the world crisis, the entrance of new countries benefiting from cheap labour and finally automation, precipitated the collapse of [even] the most prestigious watch companies and made the techniques and skills acquired over the ages by generations of watchmakers fit only for the rubbish-bin.

…

In 1983, the watch industry has reached a decisive phase of its development. Through the progress of electronics and quartz, technology is relegated to the background for the first time in history.

…

Today, the die is cast. Let us therefore forget the crisis of the technical timekeeper and turn towards the growing success of the attractive jewel which serves also to tell the time.

On May 26, 1983, the formal merger of ASUAG and SSIH was announced. The resulting Societe Suisse de Microelectronique & d'Horlogerie (SMH) led by Nicolas G. Hayek disembowelled the uncooperative management of Omega, stripped it and many others of independent decision-making, centralized control of production, slashed product lines and carried out many other painful operations. SMH would eventually rename itself the Swatch Group.

Conclusion

This relatively brief review has outlined the Swiss watch industry’s focus on advancing electronic timekeeping technology throughout the crisis. The Swiss watch industry, from 1973 and until at least 1980, counted on electronics research and development to eventually yield a national competitive advantage in market segments below the de luxe tier.

The commercial setbacks encountered while pursuing this thesis were mostly attributed to external developments such as the foreign exchange rate. While real, the doubling of the franc occurred in the context of even larger multiples of available productivity gains from automation, until competitors to Switzerland by realizing these gains had consolidated a supermajority market position by the mid-1980s.

This mistaken thesis also profoundly influenced the subsequent collective memory of the crisis.

Chapter 2, “The Watchmaking Crisis of 1975-1985”

Seiko of America was established in 1970; Citizen Watch of America in 1975.

Including predictions of future functionality amounting to a smartwatch

Conversely, a 1975 Europa Star editorial lamented the “incomprehensible demoralization [which] seems to be paralyzing some once very dynamic producers of traditional watches”

“There is no doubt now that the considerable effort made by the Swiss industry in the sector of quality electronic watches will finally bear fruit,” opined Europa Star in 1977.

As well as its belated 28,800 vph automatic caliber in the same year. Coincidence or not?

Also France and Germany.

Did this reflect an anticipation of revolutionary new types of ‘solid state’ calibers, meaning that any investments in more efficient means of producing and assembling baseplates, axles, wheels, etc. would be wasted?

Europa Star Europe | 1978 | Issue #111

“Centenary of the Swiss Watch Chamber.” La Suisse Horlogère - Édition Internationale | 1976 | 4/4

The Japanese yen was relatively stable against the US dollar in the 1970s, but this condition ended with the 1981 Plaza Accord, after which the yen also doubled in value by 1988.

Hong Kong’s annual watch export value grew by over 50 times from 1970 to 1982, according to their Trade Development Council. Movement type was a changing mix of mechanical and quartz.

There had seemed to be an implicit belief that ‘prestigious’ or ‘historic’ Swiss watch companies deserved to exist more than ‘economical’ or ‘upstart’ producers. Did this implicit hierarchy extend to overseas competitors, classifying them into ‘worthy’ or ‘unworthy’?

“The Darker the Night, the Brighter the Stars”, Europa Star Europe | 1983 |Issue #137

I ordered the book approximately 1.5 seconds after finding out that it existed from this article